Introduction

Auditing plays a central role in upholding transparency, accountability, and legal compliance in any organization. Under various regulatory frameworks, businesses—especially in the industrial, financial, and corporate sectors—are required to conduct regular audits to ensure that their financial statements, operational practices, and internal controls adhere to statutory norms and prescribed standards.

Audit requirements imposed by regulatory bodies not only validate the accuracy of financial data but also help identify risks, prevent fraud, and ensure good governance. This article outlines the audit obligations mandated under different regulatory frameworks, their types, and their significance for compliance and corporate accountability.

1. Understanding Regulatory Audits

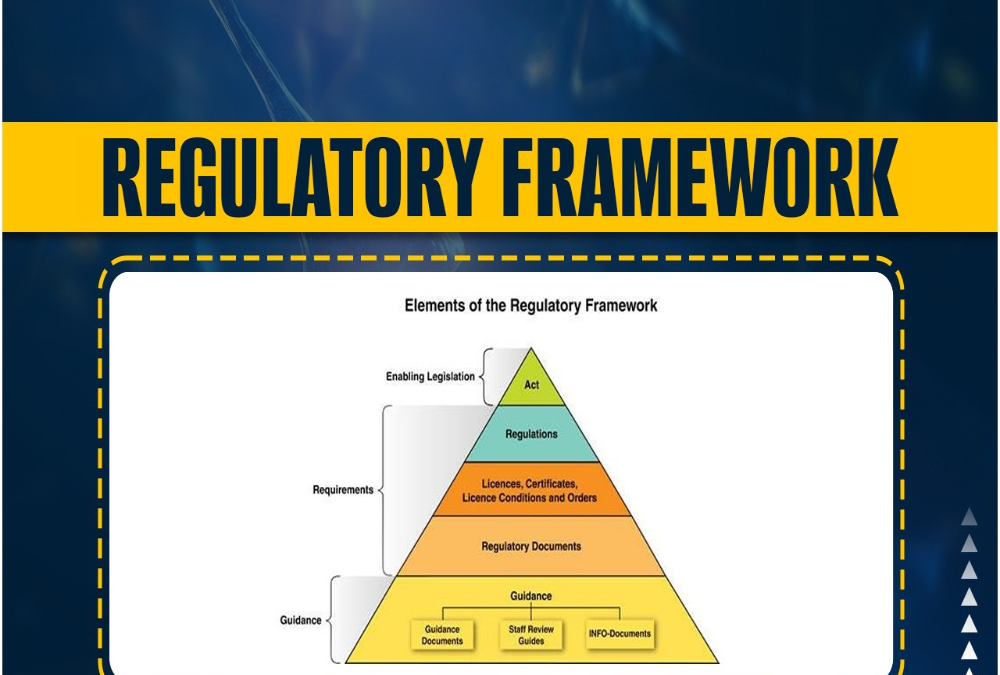

A regulatory audit is an independent assessment carried out to ensure that an organization is complying with applicable laws, regulations, and reporting standards. These audits can be mandated by government agencies, industry regulators, or financial authorities and may cover financial performance, operational practices, environmental standards, or tax filings.

2. Types of Audits Required Under Regulatory Frameworks

a. Statutory Audit

- Mandated by: Companies Act, 2013 (India), or similar corporate laws in other countries.

- Applicability: All registered companies and large partnership firms.

- Purpose: To verify the accuracy of financial statements and ensure adherence to accounting standards.

- Conducted by: Chartered Accountants or Certified Public Accountants (CPAs).

b. Tax Audit

- Mandated by: Income Tax Act (India) or tax authority regulations in other jurisdictions.

- Applicability: Businesses exceeding prescribed turnover thresholds.

- Purpose: To examine the correctness of income declarations and compliance with tax provisions.

- Form Used: Form 3CD and related annexures in India.

c. GST Audit (Goods and Services Tax)

- Mandated by: GST laws in countries with value-added tax systems.

- Applicability: Taxpayers exceeding a certain turnover threshold.

- Purpose: To verify input tax credits, tax liability, and return filings under GST.

- Requirements: Filing of GSTR-9C (reconciliation statement with audit certification).

d. Internal Audit

- Mandated by: Companies Act or required voluntarily for large entities or listed companies.

- Purpose: To assess internal controls, risk management, and compliance practices.

- Scope: Covers financial, operational, and process audits.

e. Cost Audit

- Mandated by: Ministry of Corporate Affairs (India) or equivalent regulatory bodies in other countries.

- Applicability: Industries in sectors like manufacturing, energy, and infrastructure with significant cost elements.

- Purpose: To analyze cost records and ensure cost efficiency in production.

f. Environmental Audit

- Mandated by: Pollution Control Boards or Environmental Protection Agencies.

- Applicability: Factories and industrial units with potential environmental impact.

- Purpose: To evaluate compliance with air, water, and waste management norms.

g. Secretarial Audit

- Mandated by: Companies Act and SEBI (for listed companies in India).

- Purpose: To assess compliance with corporate laws, board governance, and statutory disclosures.

- Conducted by: Company Secretaries in practice.

3. Core Objectives of Regulatory Audits

- Compliance Verification: Ensure that legal and regulatory requirements are met.

- Financial Accuracy: Detect misstatements, errors, or fraudulent reporting.

- Operational Transparency: Validate efficiency and effectiveness of internal processes.

- Risk Mitigation: Identify gaps in control systems that could lead to financial or legal exposure.

- Stakeholder Assurance: Build trust with investors, regulators, and partners.

4. Documentation and Reporting Obligations

- Audit Reports: Submitted to regulatory bodies, shareholders, or tax authorities.

- Disclosure Requirements: Findings must be disclosed in financial statements or board reports where required.

- Retention of Records: Businesses must retain audit working papers and supporting documents for specified durations.

- Certification and Filing: Some audits require certification from independent professionals and filing on government portals (e.g., MCA, Income Tax, GST).

5. Consequences of Non-Compliance

Failing to meet audit requirements can result in:

- Monetary penalties and interest

- Disqualification of directors or officers

- Suspension or revocation of licenses

- Legal proceedings or imprisonment

- Loss of investor confidence and reputational damage

Conclusion

Audit requirements under regulatory frameworks form a critical part of modern compliance systems. They not only ensure that businesses follow financial and operational rules but also promote ethical governance, accountability, and sustainable practices. For industries and enterprises, staying abreast of audit obligations and integrating them into their compliance structure is essential. As regulatory oversight continues to evolve, organizations must adopt a proactive approach to audits—treating them not as formalities but as strategic tools for improvement, risk management, and long-term success.

Hashtags

#AuditRequirements #RegulatoryFrameworks #ComplianceAudit #FinancialRegulations #AuditStandards #RiskManagement #InternalControls #ExternalAudit #RegulatoryCompliance #AuditProcess #FinancialReporting #Governance #AuditTrail #QualityAssurance #AuditDocumentation #RegulatoryStandards #BusinessCompliance #AuditBestPractices #FinancialIntegrity #CorporateGovernance